Key changes to Mandatory Quoting of Pan Rules of the Income tax Act

Rules regarding quoting of PAN for specified transactions amended

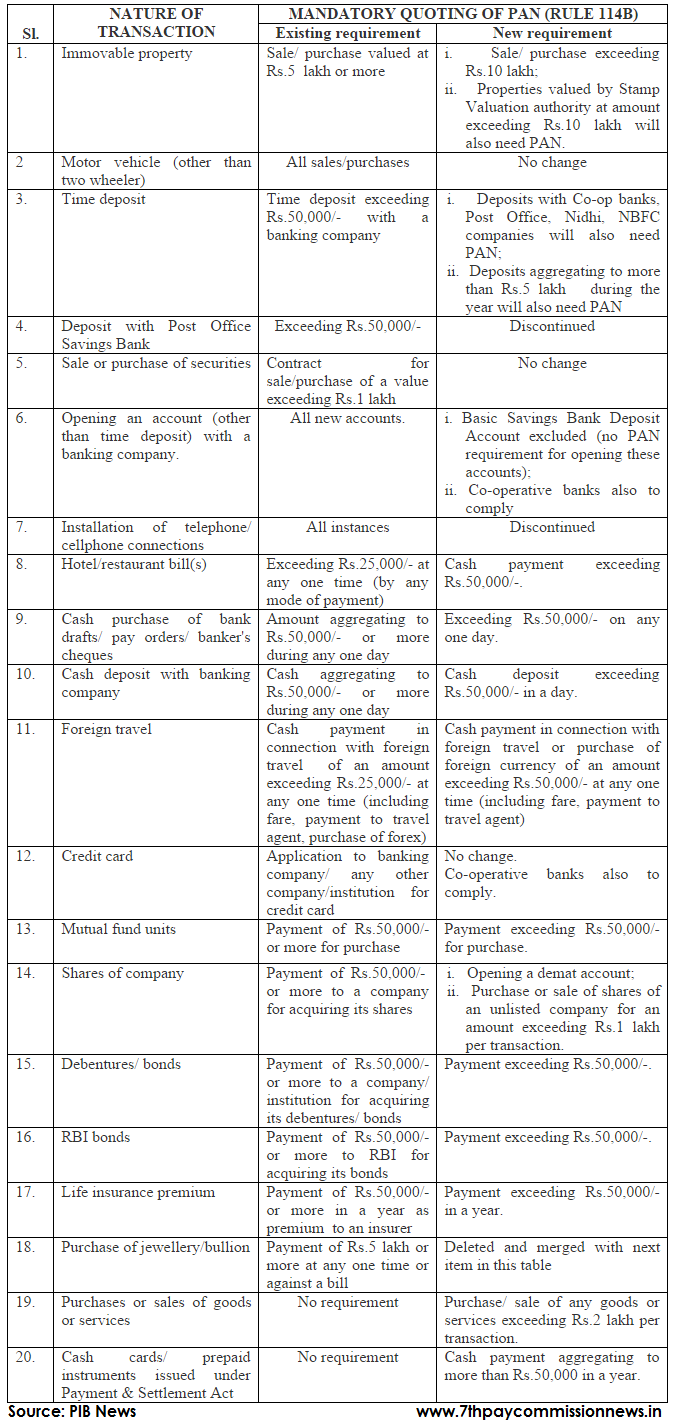

The Government is committed to curbing the circulation of black money and widening of tax base. To collect information of certain types of transactions from third parties in a non-intrusive manner, the Income-tax Rules require quoting of Permanent Account Number (PAN) where the transactions exceed a specified limit. Persons who do not hold PAN are required to fill a form and furnish any one of the specified documents to establish their identity.

One of the recommendations of the Special Investigation Team (SIT) on Black Money was that quoting of PAN should be made mandatory for all sales and purchases of goods and services where the payment exceeds Rs.1 lakh. Accepting this recommendation, the Finance Minister made an announcement to this effect in his Budget Speech. The Government has since received numerous representations from various quarters regarding the burden of compliance this proposal would entail. Considering the representations, it has been decided that quoting of PAN will be required for transactions of an amount exceeding Rs.2 lakh regardless of the mode of payment.

To bring a balance between burden of compliance on legitimate transactions and the need to capture information relating to transactions of higher value, the Government has also enhanced the monetary limits of certain transactions which require quoting of PAN. The monetary limits have now been raised to Rs. 10 lakh from Rs. 5 lakh for sale or purchase of immovable property, to Rs.50,000 from Rs. 25,000 in the case of hotel or restaurant bills paid at any one time, and to Rs. 1 lakh from Rs. 50,000 for purchase or sale of shares of an unlisted company. In keeping with the Government’s thrust on financial inclusion, opening of a no-frills bank account such as a Jan Dhan Account will not require PAN. Other than that, the requirement of PAN applies to opening of all bank accounts including in co-operative banks.

The changes to the Rules will take effect from 1st January, 2016.

The above changes in the rules are expected to be useful in widening the tax net by non-intrusive methods. They are also expected to help in curbing black money and move towards a cashless economy.

A chart highlighting the key changes to Rule 114B of the Income-tax Act is attached.

Leave a Reply